One of the people I respect the most in the VC/PE media ecosystem is Dan Primack. I’ve been an avid reader of Dan’s Term Sheet while he was at Fortune, and now Pro Rata at Axios. His writings and knowledge of the inner workings of the VC/PE ecosystem is impressive, and I have learned a lot from reading his columns over the years.

Earlier this week, Dan said something in passing which took me by surprise: “In a related note, I wasn’t really aware that pre-seed was a thing.” Reading this made me literally jump out of my chair. You see, Dan knows more about venture than most people; and if Dan isn’t aware that “pre-seed is a thing,” then I haven’t done a good enough job of explaining to the world what I and K9 do! Luckily, Kia Kokalitcheva followed up with a post titled “The rise of “pre-seed” venture capital,” that made me feel just a tad better, but that uneasy feeling still didn’t leave me.

So, I took it upon myself as a challenge to put together the definitive “Pre-Seed FAQ.” I’ll start with all the questions I can think of, from many different perspectives: founders, LPs, the press, and even other VCs. This post is intended to be a dynamic document, and I will attempt to update it from time to time with new questions that may arise or as financing trends evolve.

So, I’d like to thank Dan for shocking me into action. And I sincerely hope that this post does a good job of addressing what Pre-Seed really is.

Q: Define Pre-Seed? Or What is Pre-Seed?

Pre-Seed is the first institutional capital invested in a company. It is what Seed used to be from 2009-2013, until the Seed rounds got fat and bloated and the bar for raising a Seed round became a lot higher.

Q: What amount of financing is considered Pre-Seed?

Typically, Pre-Seed rounds are less than $1M in aggregate capital raised. Between $500K – $750K is probably the sweet-spot for a Pre-Seed round.

Q: Is Pre-Seed a Thing?

A: Yes, Pre-Seed is a thing. It’s a legitimate stage of financing in the venture eco-system as of this writing (October 2017). In practice, Pre-Seed has essentially replaced what used to be accomplished in the Seed round of funding. Today, a Seed round really accomplishes what the Series A stage used to accomplish, and today’s Series A really accomplishes what the previous… Well, you get the idea.

Q: What is the history of Pre-Seed? Where did the term Pre-Seed come from?

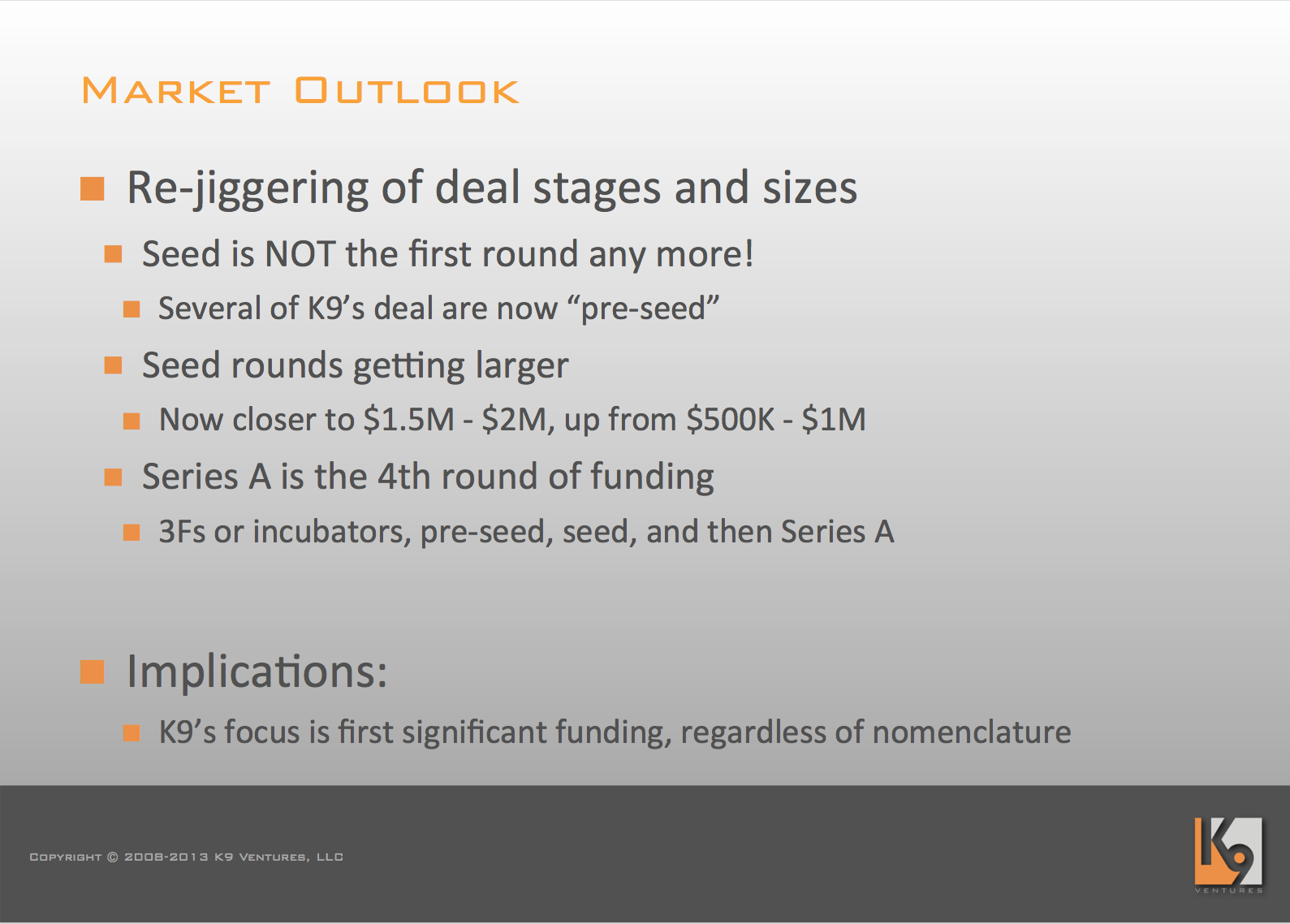

The first time I used the words “pre-seed” (yes, the initial use was in all lower-case, but then became upper-case over time) was on June 27, 2013, at the K9 Ventures LP Meeting. Here are the two relevant slides from that meeting. They talk about how deal sizes and stages were changing even back then. Seed rounds were getting bigger. Series A had become the 4th round of funding. This created a vacuum at the earliest stages of funding. Eventually, that vacuum was filled with capital gained even earlier than the Seed round — i.e., “pre-seed.”

On April 10, 2014, I published a blog post, titled The New Venture Landscape, which explained why and how the venture ecosystem was shifting. In that post I explained that:

Seed is not the first round of financing any more. In fact after noticing this trend last year, I have transitioned to calling most of my initial investments “pre-seed” rounds, where the company raises close to $500K, before raising a full seed round. The Seed round is larger — closer to and sometimes upwards of $2M. The Series A is now the fourth round of funding for a company — the first is usually friends and family, or an incubator (~$50K), then pre-seed (~$500K), then seed (~$2M), then Series A (~$6M-$15M).

As far as I can tell, that is the first public use of “pre-seed” as a stage of financing.

A follow-up post, titled The Seeds Have Changed: An Epilogue, on June 5, 2015, explained this further:

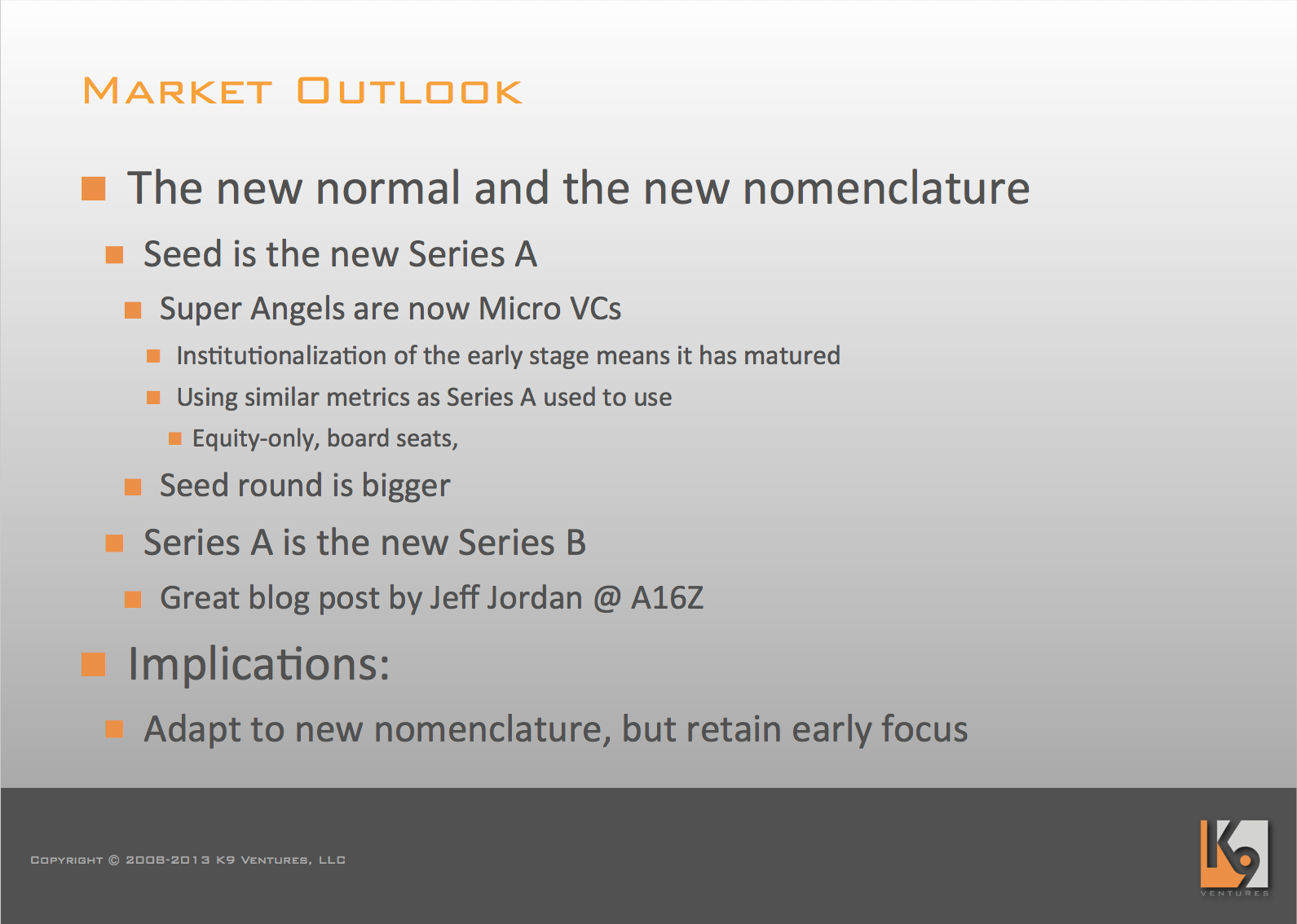

Pre-Seed is the New Seed

If the Micro-VCs are looking for Series A-like metrics, what does a company do when it’s just getting started? If it doesn’t have the product fully baked yet? Or if the traction is not yet interesting enough to attract a full Seed round? Well, enter the Pre-Seed round, where the startup raises closer to $500K.When I first started using the term ‘pre-seed’ in 2013, it was almost as a joke since I wanted to make a point that K9 was investing super early. At the time of writing the New Venture Landscape, I started to capitalize “Pre-Seed”. Over the course of the two years since, it’s been interesting to note how “Pre-Seed” has entered the vocabulary in venture. There are a now a handful of funds, K9 included, that are Pre-Seed funds in name and practice.

This has been pretty much what K9 has been doing since 2013. In fact, when I announced K9 Ventures III in August 2017, the term Pre-Seed was part of the headline for that announcement: Announcing K9 Ventures III, L.P. – A $42M technology-focused Pre-Seed fund.

Q: What characteristics does a company need to have to qualify for Pre-Seed funding?

That’s the beautiful part. A Seed round today — like the Series A round of yesteryear — requires some kind of traction or product. In contrast, you *don’t* need much to qualify as a Pre-Seed stage company. Pre-Seed investors should *not* be looking for any kind of traction. They shouldn’t even be looking for a fully built product. A prototype or a well fleshed out deck should be sufficient for a company to qualify for Pre-Seed funding.

Q: How do companies use Pre-Seed funding?

Pre-Seed financing is typically used to accomplish two things: build a team, and build an initial product and prototype.

When I first began in this industry, people would claim that it’s cheap to start a software company. Those times are long gone. It is no longer cheap to start a software company. Yes, the infrastructure is cheap (to start), but the human costs have gone up dramatically. Unless every aspect of product development is covered by founders who are only receiving equity, there are other parts of building a product that will require hiring highly qualified people. And people are expensive (especially in the Bay Area), so some Pre-Seed financing goes towards recruiting the right minimal set of people who can help to build the product.

In order for a company to attract a full Seed round ($2M – $3M), that company needs to show an almost completed product, an advanced prototype, or some kind of traction/demand metrics. Pre-seed dollars are used to create that prototype and get enough feedback on it to justify Seed investment.

As explained in The New Venture Landscape post:

Pre-Seed is the new Seed. (~$500K used for building team and initial product/prototype)

Seed is the new Series A. (~$2M used get for building product, establishing product-market fit and early revenue)

Series A is the new Series B. (~6M-$15M used to scale customer acquisition and revenue)

Series B is the new Series C.

Series C/D is the new Mezzanine

Q: Why haven’t I heard of Pre-Seed rounds before?

Most companies that raise Pre-Seed rounds do not announce these rounds. And the amounts involved are generally small enough that they don’t attract the attention of the press any way. These companies are also so early in their life-cycle that they’re not really ready to talk about what they’re working on publicly until they have something to show.

When the companies raise a Seed round where it’s now $2M+ being raised, at that stage they are closer to being ready to talk about what they’re working on — mostly because they want to attract new talent to the company. Because of this the first mention of a company in the press/media is usually concurrent with their Seed round financing announcement.

This has the effect that founders who are reading TechCrunch see headlines of the form “Company X raises $2M in their Seed round?” Add that to the conventional wisdom that the “seed” round was supposed to be the first round of funding for a company and founders start to think that that is the normal amount of capital for them to raise for an initial financing round.

It’s only when they go out to raise and find that they’re not ready to raise a Seed round, do then they learn about Pre-Seed round being an option.

Q: Is Pre-Seed subject to adverse selection? Do companies only raise a Pre-Seed when they can’t raise a Seed?

Yes and no. There are lots of companies that try to raise a $2M – $3M Seed round as their first round of financing. Some of those companies are actually successful in raising such a large initial round of financing — either because the team has a prior track record or spectacular (academic or work) pedigree. The extraordinary amount of capital flooding in at the Seed stage, often from non-traditional capital sources, foreign capital, or new funds also sometimes makes it possible for companies to raise a larger round without demonstrating the progress that seasoned investors would look for a Seed stage company today.

Of course if a company is unable to raise a $2M – $3M Seed round, a fall back plan could then be to raise a smaller sub-$1M round to get started from Pre-Seed investors. This is what creates the perception of adverse selection — that a company that couldn’t raise $2M – $3M is now raising less than $1M to get started. However, this perception is often not accurate.

The funny thing with capital is that in order for it to be effective, it needs to come in the right amount and at the right time. The company needs enough money to make progress, but if it has too much capital available it will actually end up wasting the time and capital because of the lack of focus and urgency in solving the most critical problems facing the company.

Therefore, I actually argue that companies that are successful in raising more capital, are often likely to flounder more than companies that raise the amount of capital appropriate for their stage. I’ve talked about this before in The Curse of Over Capitalization. That post was written with later stage companies in mind, but I’m now starting to see the same issues crop up in companies at earlier stages as well.

The amount of capital (and therefore the resulting valuation) also sets the stage for the next round of financing for a company. If you raise <$1M, then raising $2M – $3M in the next round feels okay. But if you start with a $3M raise, your next raise really needs to be a $5M – $6M raise. That’s squarely in Series A territory and you now need to have Series A metrics for that. So raising a larger round can almost make it harder for a company to get to that next stage of financing and puts it in a danger zone of being considered “too early” — which becomes a common reason for Series A investors to pass on a company.

In sports, you always want to play and compete at the stage that is right for you. Likewise in startups, companies need to work with the capital that is appropriate for their stage. If you try to punch beyond your weight class, your chances of getting knocked out are a lot higher.

Q: Does a Pre-Seed require founders to give up more equity in the company?

This is another common question, especially from founders who are worried about how they now have one more round of dilution to take before they get to their Series A. But when you think about it logically, if Pre-Seed is the new Seed, Seed is the new A and Series A is the new Series B, essentially all the rounds of financing have shifted. So the amount of dilution a company will take on still remains the same over the life of the company.

There is an interesting corollary here that the “life of a company” as a private company is much longer. It used to be that a company could go public when it hit $20M in revenue. Today that doesn’t happen any more and I’ve rarely seen a company that files for going public that doesn’t have over $100M in revenue. This means that companies are staying private longer and they’re raising more rounds of capital as a private company to finance their growth. So it’s normal for a company to have to raise Pre-Seed, Seed, Series A, Series B, Series C, Series D (and more) before it’s potentially ready for an IPO, but that bar for the IPO is much higher than what it used to be and the valuation of the company in private markets is considerably higher than what it used to be.

Q: How are most Pre-Seed deals structured? Notes? Equity?

Most professional/seasoned investors don’t like convertible instruments of any form. I’ve written about this on the K9 Ventures blog. Mark Suster has written about this. And David Hornik has written about this. I think Mark and David have done an even better job of addressing this in their posts than I ever could.

That said, you will find Pre-Seed deals in both flavors — Notes and Equity.

Q: What does Seed financing get used for?

Seed financing is used to finish building the product, testing for and establishing product-market fit, and developing early revenue traction. All three of those are prerequisites for a Series A.

Q: Is Pre-Seed investing more risky than Seed stage investing?

By definition, yes. The bar for the Seed round has moved up and that bar is essentially de-risking a Seed stage investment. A Pre-Seed company certainly hasn’t met the same bar. It may be a bare-bones team, with a product that is under development, with hopes of hitting product-market fit, but lacking and data points to prove that it can get there.

Investing at the Pre-Seed stage is not for the faint of heart. It requires believing in the team, believing in their vision for the future, and some amount of hope that everything will line up just the way you want it to in order for the company to be successful.

Investors in their quest to seek better (less risky, more certain) investments, invariably end up moving up The Venture Spiral — i.e. investing at later stages. Therefore I would argue that even some of the Pre-Seed investors that exist today, will end up moving up to later stages as their fund sizes grow.

Q: Is Pre-Seed only a Bay Area phenomenon?

Candidly, I’m not qualified to answer his question as I live and work inside the Bay Area bubble. So I can only talk about what I see happening here. The Seed round may still well be the first round of financing in other geographies, but in the Bay Area, it’s definitely not so.

I’d love for investors and founders from other geographies comment below to help determine if Pre-Seed is only a Bay Area phenomena, or if it’s started to show up in order eco-systems as well.

Q: Does a Pre-Seed company need traction?

No. Anyone asking a Pre-Seed company for traction or asking them about unit economics doesn’t really understand the stage at which they’re investing and they probably should be investing at a later stage.

Q: What are some Pre-Seed funds operating today?

K9 Ventures is of course a Pre-Seed fund — that’s the reason for me to be standing on the Pre-Seed soap box. In addition to K9, the following venture funds are all investing at the Pre-Seed stage:

- PivotNorth Capital

- Engineering Capital

- Precursor Ventures

- Notation Capital

- XFactor Ventures

- Afore Capital

If you have additional questions regarding Pre-Seed, please feel free to post in the comments below and I’ll monitor and update this post as needed.

You can follow me on Twitter at @ManuKumar or @K9Ventures for just the K9 Ventures related tweets. K9 Ventures is also on Facebook and Google+.

3 Comments

Hey Manu, my company MuvTix is developing a $10 monthly subscription service to help moviegoers save money each month by selling their data to enterprises and advertisers. If interested I can send you along our business plan, pitch deck etc. Thanks!

I’m not from K9, but isn’t what you are describing the same as: https://www.moviepass.com/?

Thanks for writing this Manu. As an entrepreneur, seed investors asking for “traction” has always confused me. Pre-seed needs to be known far and wide. Especially for founders looking for their first investors.